Do Economists Have Inflation all Wrong?

Economics is not like science. It doesn’t hate beautiful equations and infallible governing laws. The heart of the problem is that predictions in economics come down to people — and everyone is different...

Economics cannot predict inflation in the same way science can predict the energy release from an electron-positron annihilation. We can’t break down the wage-setting process in the same way we break down photosynthesis.

So, what can economists do?

Ed Harris' character from the 1995 film Apollo 13 summarises economic modelling perfectly. He orders his colleagues to

"invent a way to put a square peg in a round hole... rapidly."

Macroeconomists do just this. The oversimplified and outdated assumptions (square pegs) forced into their models (round holes) rarely generate correct forecasts. In truth, they just serve to provide insight into how the machinery of the economy works.

But, by being aware of how people truly think and form expectations, we can have more accurate assumptions in our models and maybe — just maybe — predict better.

In other words, we can always make the peg a little less square.

A new paper by University of Melbourne’s Sarantis (Sam) Tsiaplias, ‘Consumer inflation expectations, income changes and economic downturns’, does just this. Sam delves into how people think about and form inflation expectations in the face of a recession.

What is inflation and why do we care?

This is for those of you who don't quite know what inflation is and why it's so important.

In simple terms, inflation is an increase in prices across an economy. With some exceptions, inflation around the world is roughly 1-4%. That means if you compare prices this year to last year, on average, they will have increased by a few percent. Sam Ewing said it best,

“Inflation is when you pay fifteen dollars for the ten-dollar haircut you used to get for five dollars when you had hair.”

Inflation erodes wealth, meaning it reduces people’s purchasing power. As Milton Friedman once said,

"Inflation is taxation without legislation."

It matters for your real returns as well. These are the returns you receive after the rate of inflation is taken into account. For example, say you have a savings account paying 2% interest each year. If inflation is 1%, you earn a real return of only 1% on your savings. However, if inflation rises to 3%, your nominal return is still 2%, but you are now making a real loss of 1%.

The great irony is that our expectations of inflation largely dictate inflation. Suppose the majority expect prices to rise significantly next year (i.e. expecting a high level of inflation). In that case, they will want to maintain their real incomes. In order to do so, they will push for a wage rise at least as great as what they are expecting the price rise to be. Businesses, however, need to maintain their profit margins. So, they will raise the prices of their products to afford the wage rises of their employees.

Now, how do people predict next year’s price rise? Well, that is a great question; it is precisely the question this paper answers.

The square peg

Most academics assume people expect inflation to simply be the same as last year. If everyone thinks this way, inflation follows the Phillips Curve. This is inflation theory's 'square peg'.

The Phillips Curve is an identity relating inflation and economic growth. It argues when growth rises, inflation also rises and vice versa.

So what does this mean for inflationary expectations? It means when aggregate income rises due to economic growth, inflationary expectations rise.

The Phillips Curve is not a law. It is not like Newton's three laws of motion. In fact, there is little evidence for it existing.

However, it does still provide insight. Although the Phillips Curve is a square peg in a round hole, it still allows economists and policy-makers to better understand the ‘macro machine’.

Why could this be wrong?

When asked "What do you expect inflation to be in one year?" almost everyone (bar the economists out there) don't know where to start.

Instead of answering this question, many will substitute it for a much simpler one. The question people actually ask themselves determines their expectations of inflation and in turn impacts what inflation will be.

Here's a breakdown of two inflation heuristics people can subscribe to. Basically, these heuristics are the question substitutions we just mentioned.

The Phillips of the world swap "what do you expect inflation to be?" with something along the lines of "are my wages increasing and is the economy going well?". The reason we called them 'Phillips' is because their expectations of inflation follow the Phillips curve. If their income suddenly falls, they are now absolutely poorer and therefore expect inflation will fall. Traditional economics assumes everyone is a Phillip.

The John Citizens of the world swap "what do you expect inflation to be?" with the question "what is happening to my purchasing power?". Therefore, a relative income fall feels exactly the same as a general price rise. In other words, if their income falls, they expect inflation to rise.

These two types of people have the opposite expectation for inflation, just by using different heuristics.

It should be noted this explanation was not part of Sam's paper, but we feel it nicely introduces the psychological reasons for individuals having different inflationary expectations.

How do we make the square peg a little bit rounder?

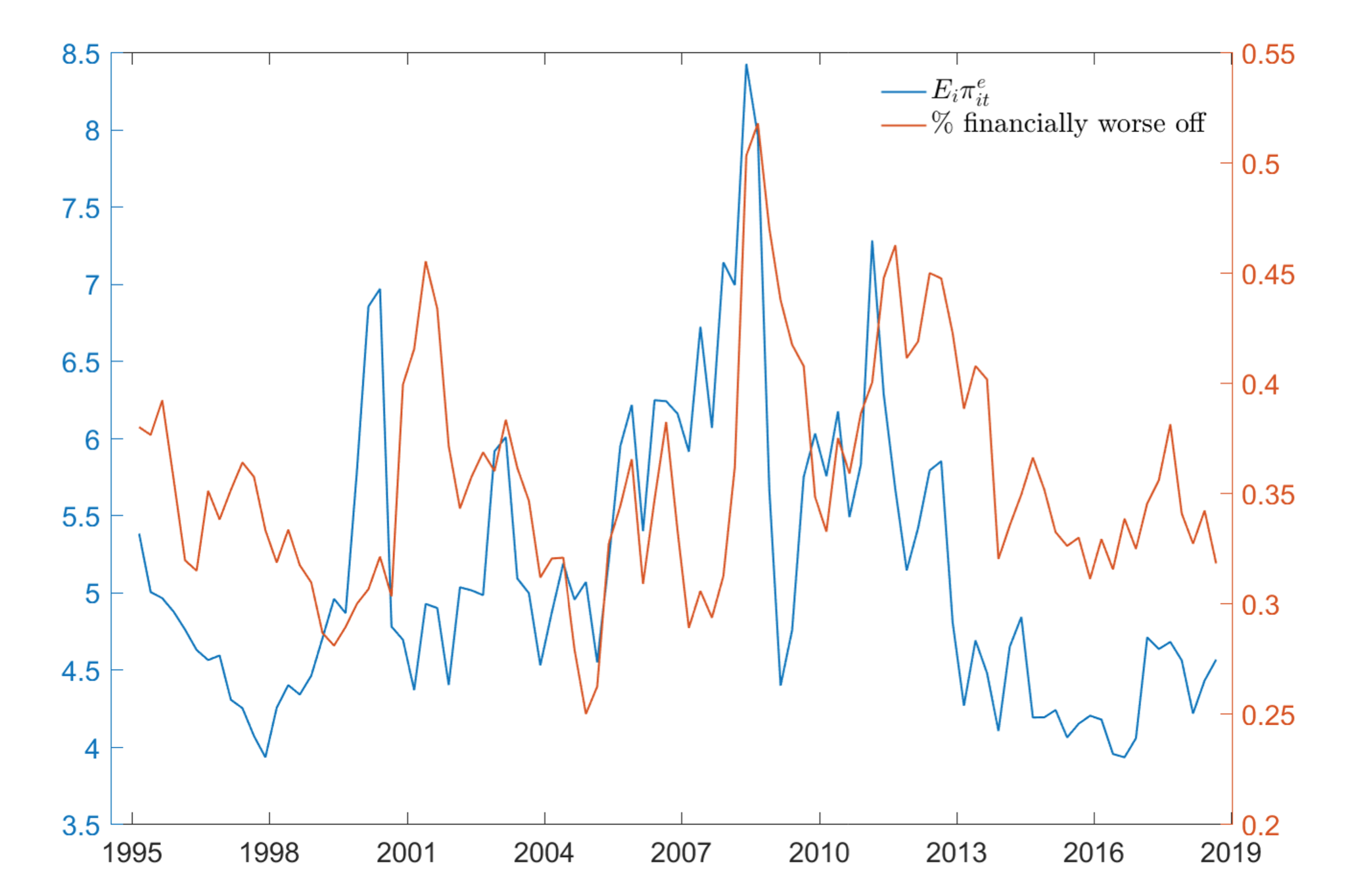

In essence, the paper shows many people aren't our Phillips, but are actually our John Citizens. Have a look at the graph below; the blue line represents the average inflation expectation and the orange line is the proportion of people who's income has dropped in the past month.

As you can see, there is a strong correlation between the two lines. That means, for many people, income falls are followed by rising expectations of inflation. In fact, the paper predicts around 20% of the Australian population sets their inflation expectations like our John Citizen. This directly contradicts the Phillips curve’s prediction that expectations should always fall with dropping income.

I know what you are thinking: this correlation could be explained by many other factors such as demographic characteristics, education level, economic optimism and whether they watch the news. One of the big successes of the paper is that it removes these confounding effects and still shows many people who lose income expect inflation to rise.

You may be asking: are there any common characteristics of the John Citizens? We asked Sam this, and he said they are typically low-income earners and non-professionals.

It's best not to think of the defining characteristics of a John Citizen, but instead simply ask the question: who is more likely to suffer large drops in income?

What does this research mean?

If there is one thing to remember with macroeconomics, it is that the insights are entirely dependent on the assumptions we make. As a result, square pegs in round holes prove to be a big problem. If our assumptions of inflation are too rigid, and often invariably wrong, the 'macro machine' can fail even to give insight.

When we spoke to Sam, he agreed and said, "Economics has assumed too strict assumptions on how to think about prices".

Two questions immediately came to our mind:

Only 20% of people are 'John Citizens'. That doesn't sound like that many people, so does this really have an impact?

Even if they do have an impact, could these opposing expectations somewhat cancel out and help temper the movements in inflation?

Sam believed these questions deserved their own research papers. Aggregating behaviours is complicated, and without careful consideration, can produce incorrect predictions.

In saying this, Sam believed the 20% did have an impact. He said, the data shows when there are many adverse income shocks, inflation volatility spikes. This leads to greater uncertainty for everyone over where inflation is and where it will go. In a field already as uncertain as macroeconomics, more uncertainty is never a good thing.

However, Sam was not so sold on the second question. He said "it may be the case that the two inflationary expectations somewhat offset each other", but was unsure either way.

One thing is certain, government bodies and policymakers – especially the RBA – have to start considering the John Citizens when they are forecasting inflationary expectations. Then, the square peg will become a little more round.

Final thoughts

Economic models are theoretical fabrications. They provide insight into the world but often struggle to accurately predict it. Sometimes we are even forced to build models to fit the description we want.

Even Jerome Powell acknowledged the ‘squareness’ of the Phillips Curve,

"The persistent shortfall in inflation from our target has led some to question the Phillips Curve...[It] has weakened over the past couple of decades.”

Sam's paper improves our understanding of how people form expectations on something as complicated as inflation. However, implementing Sam's approach into our 'macro model' is far from easy.

For the time being, square pegs in round holes might just have to do...

A more detailed discussion (Additional reading)

This is an extra section to the articles at the end to explain any simplifications we made, discuss more intricately complex parts of the paper and introduce any extra thoughts we have on the academic implications of the work.

The last two years provide an interesting case for what happens when many people suffer sudden income falls. The initial lockdowns tanked the global economy in early-mid 2020, causing the incomes of millions of individuals to fall suddenly and sharply. The Phillips expected inflation to fall while the John Citizens expected inflation to rise. Generally, inflationary expectations did fall, but they rebounded quickly (along with inflation) and remained incredibly volatile.

In Australia, the governments ‘JobKeeper’ and ‘JobSeeker’ responses greatly alleviated the income falls seen in other countries. An unexpected but beneficial side-effect of this intervention could have been a shrinking of the volatility of inflation by limiting the inflationary uncertainty of consumers.

Whether this is true is certainly up to debate. We will let you decide this for yourself. However, if this was true, it certainly allowed the RBA to better anchor inflationary expectations – crucial to ensuring economy-wide price stability.

More from Academia Unveiled:

Alternative data is taking the financial world by storm